What You Need to Know About the Latest FICO Score Changes

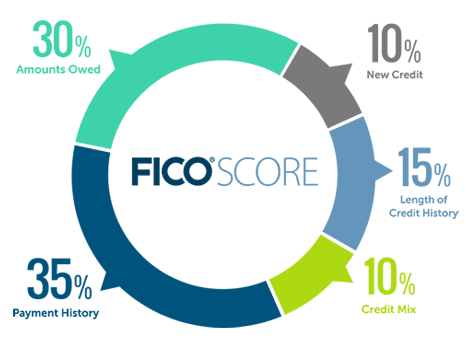

The Fair Isaac Corp (FICO) scoring model is a calculation of various pieces of credit data by which your three-digit credit score is based. The term “FICO score” can be used for a wide range of different scores provided by the company because there are several active versions of the scoring model. Every few years, the company updates or changes the way the score is calculated.

Coming this Summer, FICO is releasing two new credit scores, the FICO Score 10 and the FICO Score 10T. FICO suggests that by adopting the FICO Score 10 Suite, a lender could reduce the number of defaults in their portfolio by as much as ten percent among newly originated bankcards. The reduction in defaults is even higher for newly originated mortgage loans, at 17 percent compared to the current version used by that industry.

The FICO Score 10 will place more emphasis on personal loans, penalizing borrowers who take on personal loans to consolidate credit card debt and then choose to rack up more debt. The FICO Score 10T will look at “trended data” for the past 24 months to see how a borrower is managing their debt and will reward people who are working to pay off their debts but could cause people’s scores to drop if they have taken on more debt over time.

These models will likely help people with high credit scores have even higher scores and those with lower scores fall a little lower producing a bigger gap between low and average to high scores. It’s important to note that many lenders are still using old models, and this may not affect many people right away but as lenders start to transition it will be a bigger deal.

Check out our Facebook Live Video on this topic below.