Financial Stress Forecast

Financial Stress

Among Consumers

Financial stress, a pervasive issue affecting many individuals, can lead to anxiety, depression, and even physical health problems. The Financial Stress Forecast and Debt Burden Scale are invaluable tools for understanding the extent of this problem and predicting potential economic downturns. By providing insights into Americans’ financial behaviors and attitudes, these metrics enable policymakers, financial institutions, and individuals to take proactive measures to mitigate financial hardship and promote overall economic stability.

The Current Forecast

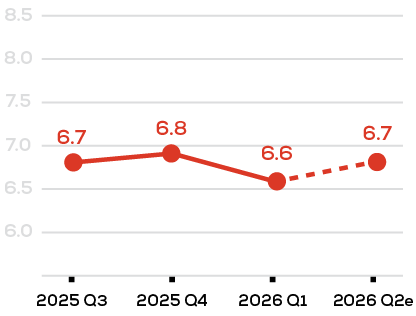

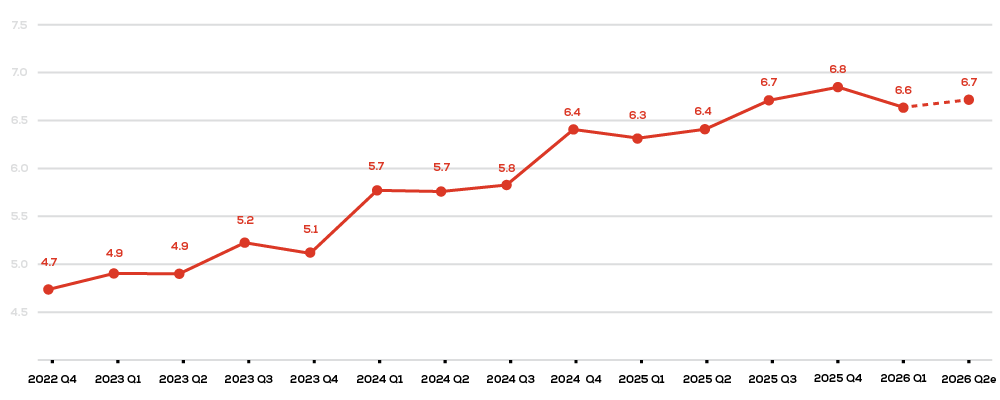

The NFCC FINANCIAL STRESS FORECAST (FSF) eased slightly to 6.6 in 2026Q1 and is projected to edge back upward to 6.7 in 2026Q2, indicating that households remain locked into a sustained period of elevated financial strain. While the recent flattening of the forecast may appear to signal stabilization, stress levels above 6.0 reflect an environment in which debt continues to constrain everyday financial choices, limit flexibility, and suppress

savings capacity. Rather than improving, the persistence of the FSF within the 6.4–6.8 range suggests that high consumer financial stress has become entrenched. Compared with the post-pandemic low near 3.5 in 2021, the current forecast points to a markedly tighter and more financially constrained consumer landscape.

Key Insights from the Q2 Forecast:

- Entrenched Financial Stress: The FSF measured 6.6 in 2026Q1 and is projected to remain elevated at 6.7 in 2026Q2, indicating that households continue to operate under sustained financial pressure with little evidence of meaningful relief.

- High Stress Plateau: The recent leveling of the FSF between 6.4 and 6.8 does not signal improving conditions. Instead, it suggests that consumers are becoming stuck in a prolonged cycle of elevated debt burdens, constrained cash flow, and reduced financial flexibility.

- Long-Term Deterioration in Household Conditions: Compared with the post-pandemic low near 3.5 in 2021, the FSF remains nearly double its trough level, pointing to a materially weaker consumer financial position and heightened exposure to future delinquencies and repayment stress.

The Forecast History

How it works.

The NFCC Financial Stress Forecast can predict delinquency rates among consumers with credit card debt.

It gives insight on the federal reserve delinquency and charge off rates for the upcoming quarter with 95% accuracy.

The NFCC Financial Stress Forecast serves as a critical early warning indicator of potential economic instability.

National Foundation

for Credit Counseling

Founded in 1951, the National Foundation for Credit Counseling is the oldest nonprofit dedicated to improving people’s financial well-being. With 1,215 NFCC Certified Credit Counselors serving 50 states and all U.S. territories, NFCC nonprofit counselors are financial advocates, empowering millions of consumers to take charge of their finances through one-on-one financial reviews that address credit card debt, student loans, housing decisions, and overall money management.